Life Science Outsource Advisor - July 2020

SEA is pleased to provide our Life Science Outsource Advisor – dedicated to keeping our readers up to date on key developments in the world of mergers and acquisitions for outsource providers to the Life Sciences industry.

Executive Summary

The rise and fall (and rise) of vertical integration in Life Sciences…

Prior to the 1980s, the Life Sciences industry was dominated by large, vertically integrated pharmaceutical companies. Everything from early stage drug discovery through clinical operations to commercialization was handled in-house. Competitive pressures forced the industry to take a hard look at the inefficiencies inherent in this “one-stop-shop” approach. Many areas with variable workloads (such as clinical trials management) were outsourced to smaller specialists who could do the work better, faster, and cheaper. This pattern of outsourcing fueled itself. As big pharma reduced headcount through outsourcing, displaced employees grew the outsource industry, allowing pharma to outsource even more. The Life Science Outsource industry grew rapidly as the large biopharmaceutical companies focused on their core capabilities.

More recently, industry dynamics are forcing the outsource industry to rebuild much of what big pharma spent decades dismantling. Large biopharma companies continue to move more of their purchasing decisions to procurement departments, many of which look to reduce the number of vendors they work with. This allows them to negotiate more favorable pricing and terms by increasing the volume of work that they direct to an individual vendor. This dynamic, coupled with consolidation among many of the large Life Science companies has left the outsource providers with a need to expand their offering to meet growth objectives. This has been a primary driver of M&A activity among the big outsource providers as they look to acquire additional services to sell to their biopharma clients. Much of this has been led by the major CRO’s who are attempting to integrate vertically and become “one-stop-shops” for their biopharma clients. Sound familiar? Time will tell how long this cycle will last but growth and diversification of services through acquisition appears to be a trend we expect to continue for the foreseeable future.

Spotlight on Contract Research Organizations

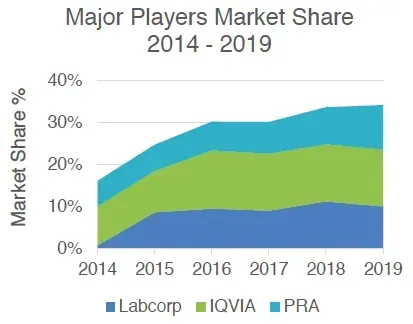

Market Conditions (Source: IBISWorld)

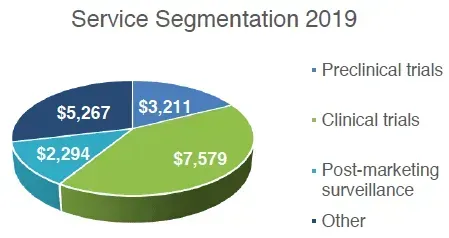

The US CRO industry has experienced strong growth over the five years to 2019, benefiting from rapidly increasing R&D expenditures. Industry revenue grew at an annualized 6.1% to $18.4 billion during the five-year period, including growth of 3.8% in 2019. During this same period, total R&D expenditures increased at an annualized rate of approximately 3.0%. Given the increasing costs of drug development, there is high demand for the services provided by CROs. Many pharmaceutical companies have lost revenue due to patent expirations, driving them to outsource aspects of the drug development process to CROs to reduce costs. However, the industry is beginning to show signs of maturing, with industry revenue growth slowing in recent years. Over the past five years, the CRO industry’s largest players engaged in a series of consolidations and actively courted strategic partnerships with pharmaceutical companies.

Prior to the COVID-19 pandemic, IBISWorld was forecasting revenue growth for the CRO industry to slow slightly but remain relatively robust, driven by anticipated increases in industry R&D spending. Since the beginning of the pandemic, numerous clinical trials were halted or scrapped as patient engagement became impractical or dangerous and the industry’s focus shifted to finding treatments and a vaccine for COVID-19. It will be some time before any realistic forecasting can be done for the CRO industry but you can expect the focus of services and offerings to shift based on what the industry learns about attempting to manage clinical trials through a global pandemic.

According to IBISWorld, the following trends will be key dynamics impacting the CRO market:

- The industry has expanded at a rapid pace by moving toward a full-service model

- The growth of a few dominant operators has led to an increasing level of concentration

- The biomedical field is likely to play an important role in the continued success of CROs

- Strategic partnerships are expected to increase over the next five years

- The push toward strategic relationships will keep industry consolidation relatively high

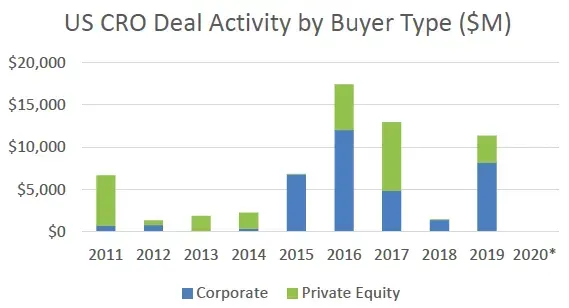

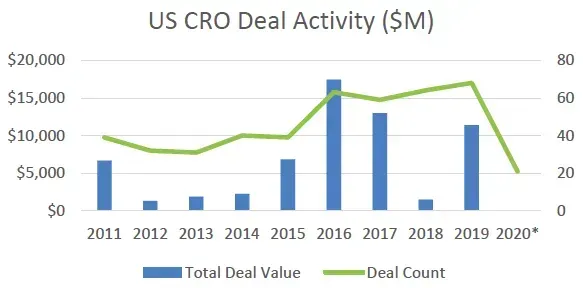

M&A Landscape (Source: Pitchbook data)

The US CRO M&A Landscape has been robust over the last decade with several outliers in the data worth noting:

- In 2011, PPD was acquired by The Carlyle Group for $3.9B through a public-to-private LBO.

- 2015 saw Labcorp’s entry into the CRO market via its $6.1B acquisition of Covance.

- In 2016, the $10.4B merger of Quintiles and IMS Health, Cinven’s $1.4B acquisition of Bioclinica and inVentiv Health’s sale to Advent International for $1.9B drove the market.

- 2017 was marked by Parexel’s $5B public to private acquisition by Pamplona Capital Management and the $4.3B merger of INC Research and Inventiv Health to form Syneos Health.

- In 2019, the major deals of note were the sale of Medidata to Dassault systems for $5.6B and the $3.2B LBO of WIRB – Copernicus.

The first half of 2020, with the onset of the COVID-19 pandemic, has experienced a dramatic slowing of M&A activity for the CRO industry. While this somewhat aligns with an overall slow-down in M&A activity in the first half of 2020, the industry wide disruption in clinical trials has likely amplified the impact of the shutdown on the CRO industry. While the broader M&A market is optimistic for a strong second half of 2020, the CRO market may be slower to move until there is more clarity around restarting/resuming clinical trials.

* through June 30, 2020

Market Movers

The companies profiled below represent some of the most active Strategic Buyers in the CRO Market based on the number of acquisitions completed during the last twelve months. These are currently some of the most acquisitive companies in the CRO industry:

WIRB–Copernicus Group (WCG) offers services in the areas of clinical and human gene therapy research, laboratory bio-safety consulting, human research protections, clinical research support and online learning. WCG completed 3 acquisitions during the last twelve months including PharmaSeek in August 2019, Waife & Associates in November 2019 and Statistics Collaborative in January 2020.

ICON provides contract clinical research services to the global pharmaceutical industry and manages clinical studies in addition to providing data management, regulatory, and central laboratory services. ICON completed 2 acquisitions during the last twelve months including Symphony Clinical Research in September 2019 and Medpass International in February 2020.

Charles River Laboratories is a provider of drug discovery and development services and is the leading provider of animal models for laboratory testing. About half of the company’s revenue comes from drug discovery and preclinical testing, and one fourth comes from the manufacturing support segment. Charles River completed 3 acquisitions during the last twelve months including Hainan New Source Biotech in August 2019, PathoQuest in September 2019 and Hemacare in January 2020.

Velocity Clinical Research provides support to the pharmaceutical, biotechnology, and medical device industries in the form of research services outsourced on a contract basis. Velocity completed 4 acquisitions in the last twelve months including Rapid Medical Research in November 2019, Advanced Clinical Research in November 2019, Omega Medical Research in June 2020 and Buynak Clinical Research in June 2020.

IQVIA is the result of the 2016 merger of Quintiles and IMS Health. The CRO segment focuses primarily on providing outsourced late-stage clinical trials for pharmaceutical, device, and diagnostic firms. IQVIA has completed 7 acquisitions in the last twelve months, most notably the $200m acquisition of GCE solutions, a CRO serving the bio-metrics sector in September 2019.

About Strategic Exit Advisors

Strategic Exit Advisors is an investment bank focused on mergers and acquisitions in the Life Sciences and B-to-B Services sectors. We help CEOs with company revenues of $5 to $100 million. We the same rigorous M&A process that Fortune 500 companies enjoy to firms your size (www.se-adv.com). Let’s talk.